New homeowner platform innovation

A discovery project with a lean testing approach focused on concept testing for idea iteration.

Project type: Concept testing and idea iteration workshops

Period: 1 month project conducted in December, 2021

My Role and Team: Project lead UX researcher, paring work with a product owner

1.The Project Background

Traditionally, banks in Thailand have heavily focused on providing a physical mortgage experience. Prospective home buyers usually receive loan options from either the property developer’s salesperson or the bank’s loan salesperson. Typically, they need to apply for mortgages with 3-4 banks before deciding on one. This entire process can take 1-3 months, with property appraisals costing between 3,000 and 5,000 THB per bank.

The PROBLEM STATEMENT

Recognising an opportunity for digital transformation, Siam Commercial Bank aimed to digitise parts of this process to become a digital-led banking service provider.

2. The methodology

The HOW

As the lead UX researcher for this project, I chose to employ a lean ideation and validation approach due to a constrained research discovery timeline of one month. This lean approach covered the following activities: A) Aligning vision B) Ideation C) Two round tests and idea refinement D) Shaping the first MVP of the product

A. Aligning the vision

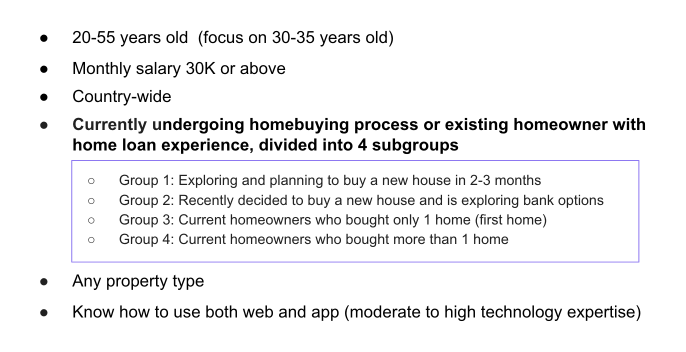

Proto personas

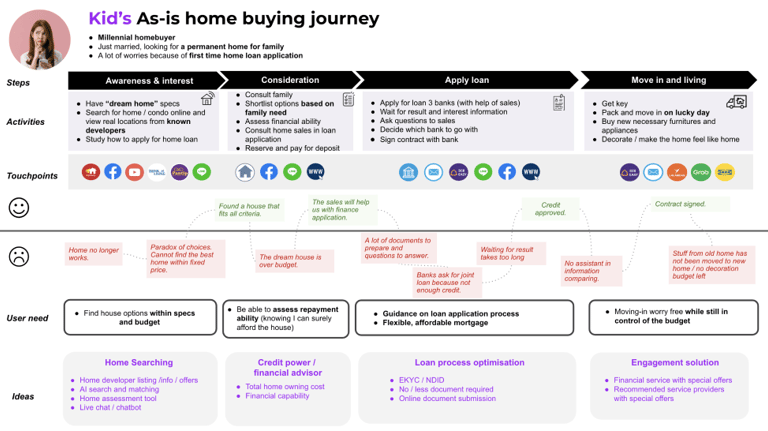

To identify potential homeowner groups, the research team conducted secondary research, utilising existing market research reports to narrow down the demographics and expectations of homebuyers both globally and domestically. This analysis resulted in the identification of four proto personas, each with distinct goals and needs.

To further understand process and pain points of the homebuyer, I conducted a guerrilla user interview with a few people in each persona group so that the journey can be more refined in detailed for the ideation activity.

Competitor analysis and market research

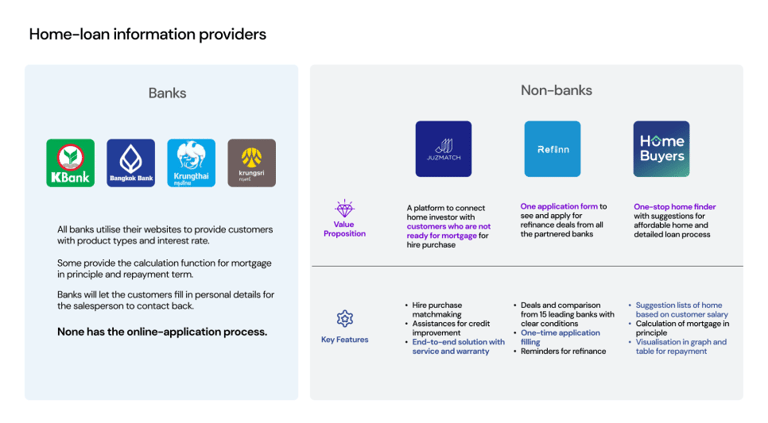

With an initial product vision of creating a one-stop digital service for mortgage customers, the UXR team conducted market research to determine if any other banks had digitalised these processes and, if not, what alternative solutions customers were using.

Our findings revealed that while all banks have digitalised the mortgage process at the initial stage, allowing users to search for loan options online, the actual application process remains offline, handled by salespersons interacting directly with customers.

We also identified several home search platforms offering supplementary services such as calculation tools, refinance applications, and hire purchase matchmaking. However, no bank or platform provided a fully online process for first-time mortgage applications, nor a comprehensive service for homeowners.

Recognising this market gap, stakeholders agreed to explore opportunities around an end-to-end self-service platform for homeowners, from the initial house purchase to ongoing homeownership needs.

B. Ideation

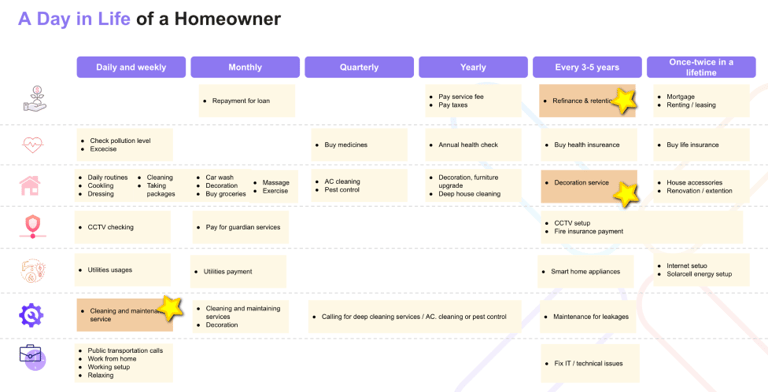

Brainstorming session: A day in a life of the homeowners

To develop compelling features and increase the likelihood of users switching to our platform, we took a step back to gain a deeper understanding of the home user ecosystem. This led us to identify and focus on three key opportunity areas.

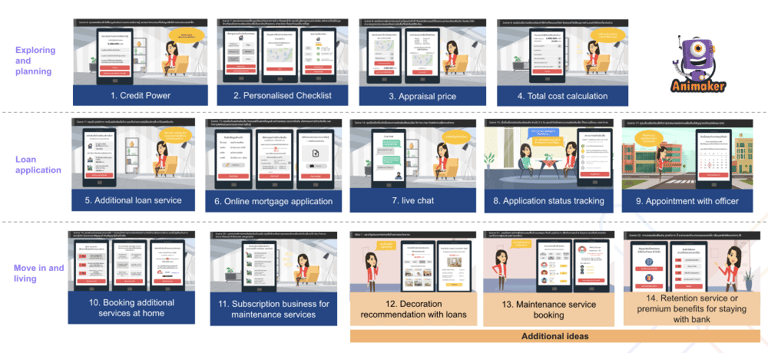

As a result of the workshop, we identified 14 ideas to further develop into design concepts for testing with customers.

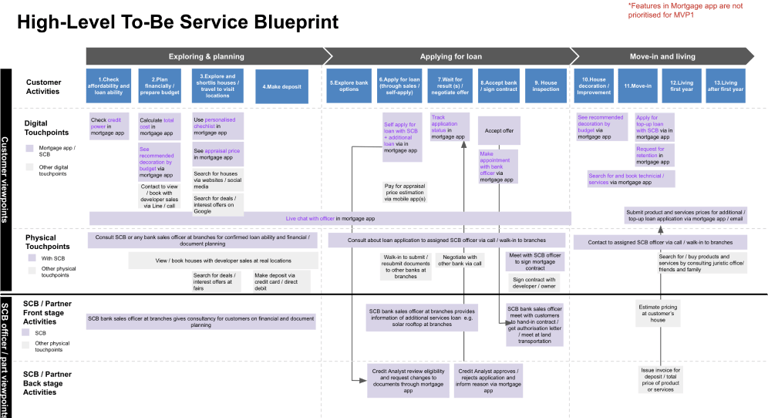

The to-be service blueprint

To help paint a picture of the holistic experience, I created a "to-be" service blueprint. This blueprint encompassed both digital and physical interactions that customers would encounter, based on the assumption that the digital solution would operate alongside the traditional physical service.

The concept storyboard

To help paint a picture of the holistic experience, I created a "to-be" service blueprint. This blueprint encompassed both digital and physical interactions that customers would encounter, based on the assumption that the digital solution would operate alongside the traditional physical service.

C. The Concept Tests

Testing round 1

After securing 9 participants for the first round, I conducted 1.5-hour online research sessions via Google Meet with each of them.

The session started with a 30-minute interview to familiarise myself with the participants' personas and gather their current journey experiences. This helped validate the initial journey maps created from the guerrilla interviews.

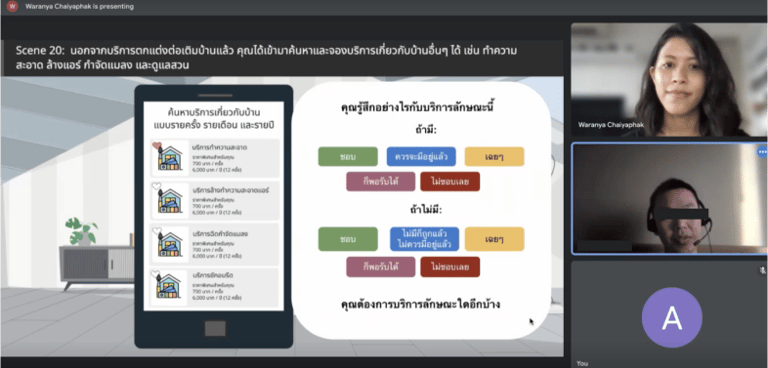

Following this, I spent another 45 minutes conducting concept tests.

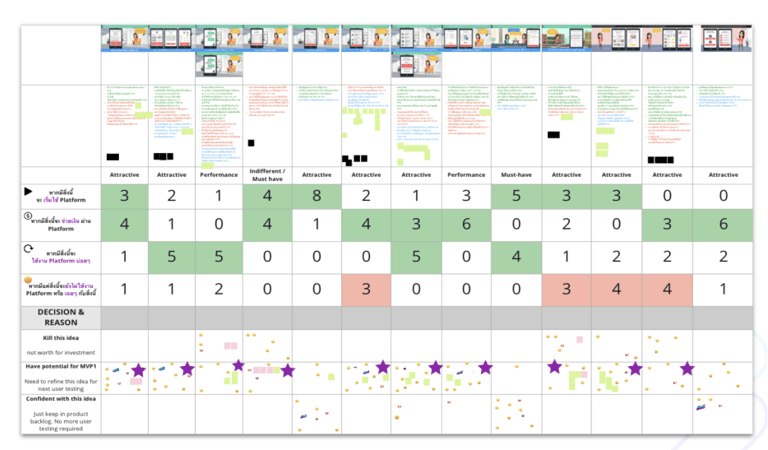

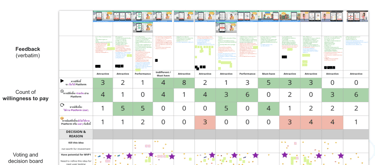

During this phase, I presented the participants with concept ideas using key screen examples. I utilised the KANO model alongside qualitative feedback to assess each concept's potential and impact.

Finally, I spared the last 15 minutes for feature prioritisation using card sorting technique, asking the participant to sort the most valuable feature for them to help shortlist MVP features.

Key Findings from Round 1 Test

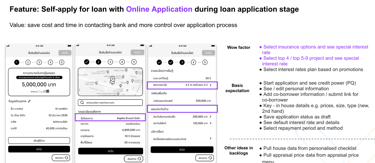

1. Online is better only if it provides the same service value as in-person

The features users valued most were those that automated the entire mortgage application process, including total cost calculation, online application, and retention requests. However, feedback revealed that these online services must offer transparency and efficiency in delivering necessary information, much like the clarity expected from in-person services. If users feel that retrieving hidden or unclear information takes longer online than in person, they may still prefer in-person interactions.

2. First-time buyers (intenders) appreciate an all-online service, as it reduces stress in information gathering

Among various user groups, the self-service online process was particularly well-received by first-time homebuyers. This group values the platform for reducing research time, alleviating stress from interacting with multiple bank salespeople, and offering the convenience of online retention requests.

To help stakeholders better understand this customer group, I analysed interview data and created a detailed persona representing the potential user of the platform.

Testing round 2

Moving forward, I organised a checkpoint with stakeholders to thoroughly review the customer persona and discuss customer feedback on each idea.

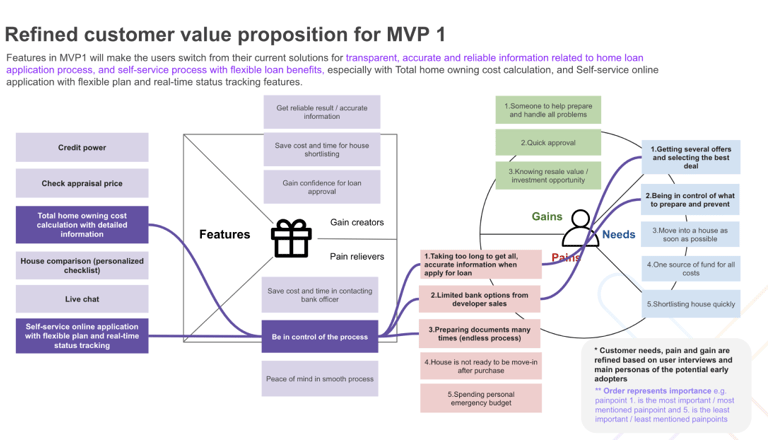

Having identified the potential platform adopter group, the value proposition was refined to better cater to the needs of first-time home buyers looking to secure their first house.

As a result, 4 out of the 14 ideas were adjusted to align with the updated value proposition.

Idea adjustment

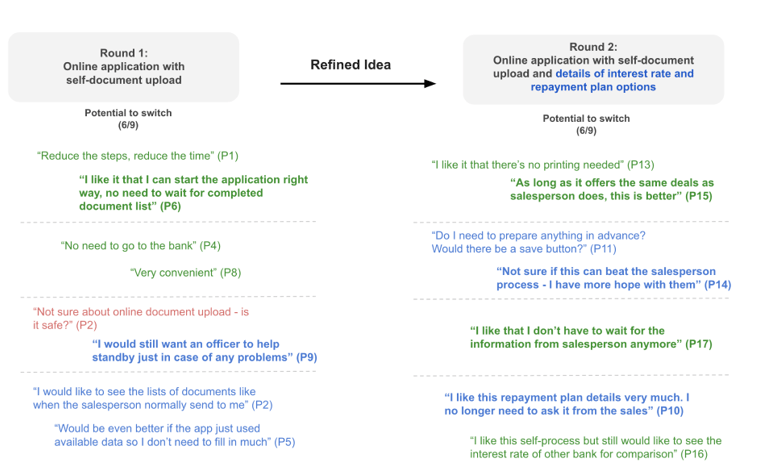

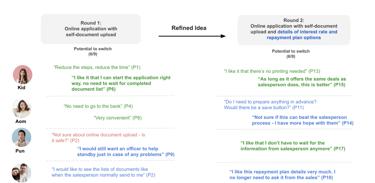

After refining the ideas and conducting a second round of testing with a new set of participants, the team reviewed the feedback together. Certain elements emerged as must-haves for customers to consider using the platform.

For instance, in the online mortgage application feature, participants from the first round expressed enthusiasm for the paperless process, which saves time and costs associated with printing and contacting bank officers. However, they also voiced concerns about the one-way interaction and the lack of essential information typically provided by a bank's salesperson, such as detailed interest rates and repayment plans.

In response, during the second round of testing, we incorporated these details into the feature. This adjustment resulted in immediate positive feedback.

Consequently, we recommended a solution that maintains a clear and guided application process, offers transparent information on mortgage terms, and ensures continuous support throughout the process.

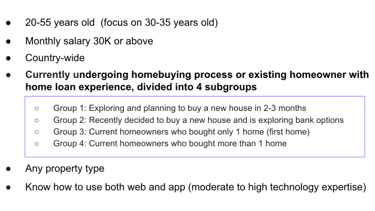

The WHO & The CHALLENGE of recruitment

The participant criteria were based on the proto-persona demographics. To gather comprehensive feedback from various home ownership journeys, the UXR team decided to recruit a diverse sample of participants at different stages of the home ownership process.

Given the project's need for a short feedback loop for iteration, I began recruiting participants that fit the proto-persona groups using a social media platform. Since Facebook is a popular information-seeking tool in Thailand, I joined home loan groups and posted a recruitment flyer detailing the criteria and compensation to encourage sign-ups.

5. The outcome

A workshop to help define MVP

After completing a one-month discovery phase and analysing the results, I facilitated a workshop with representatives from product owners, developers, and the QA team, with aims to assess the feasibility and intricacies of each feature, to be put in the first MVP.

Product requirement document

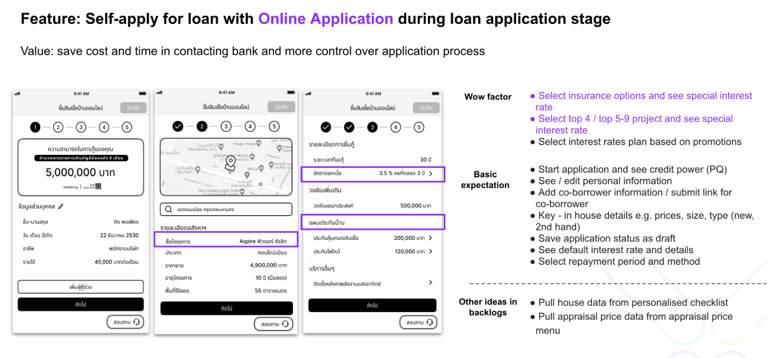

Together with the workshop participants, we came up with a product requirement document outlines both fundamental expectations and standout features of an online mortgage application process, informed by customer feedback. Accompanying wireframes were created to visually depict key features, facilitating management review and technical capacity estimation thereafter.

6. My personal takeaway

1) Lean ideation drives focused innovation

The application of lean ideation in this project was a key factor in keeping the team focused on delivering a practical, viable product. By starting with a clear problem statement and rapidly brainstorming a range of potential solutions, we were able to filter ideas based on feasibility and impact. This approach minimised time spent on ideas that didn’t align with user needs or project goals, ensuring that we could focus on the most promising concepts to move forward with.

2) Lean methodology reduces risk and uncertainty

By applying lean ideation and testing, we minimised the risks of developing a product that didn’t meet market needs. Iterative testing and feedback loops helped us make decisions quickly and adjust the product based on insights, reducing the chances of costly missteps. This approach highlighted the importance of flexibility in product development, allowing us to pivot and refine ideas rapidly without losing momentum.

3) Challenges in recruiting participants for rapid testing

One of the challenges we faced during the rapid testing process was recruiting participants who were representative of new homeowners. Given the specific nature of the target audience, it was sometimes difficult to find and engage users who could provide relevant, timely feedback. The recruitment process took longer than expected, which impacted the speed at which we could run tests and refine the product. This highlighted the importance of having a solid participant recruitment strategy and network in place to ensure smooth testing phases, especially when working under tight timelines.

Anya Hemtanon

Crafting user experiences with a lean approach

anyahem.info

© 2024. All rights reserved.